When it comes to safeguarding your vehicle, comprehensive car insurance stands out as one of the most robust options available. Unlike basic liability coverage, which only protects against damages you cause to others, comprehensive insurance offers a wide range of protection for your own vehicle. This type of policy covers various scenarios, from natural disasters to theft, providing peace of mind for car owners. In this article, we will delve into what comprehensive car insurance coverage options entail, how they work, their features, pros and cons, alternatives, and provide a final verdict on whether this coverage is right for you.

What is Comprehensive Car Insurance Coverage?

Comprehensive car insurance coverage is an extensive policy that protects your vehicle against damages that are not the result of a collision. This includes a wide array of potential risks such as theft, vandalism, fire, natural disasters, and more. Essentially, comprehensive coverage acts as an all-encompassing safety net for your vehicle, covering many of the unexpected events that could cause significant financial loss.

Unlike collision insurance, which covers damages resulting from accidents with other vehicles or objects, comprehensive insurance covers incidents beyond your control. This makes it an attractive option for those looking to ensure their vehicle is protected against a broader range of potential threats.

How Comprehensive Car Insurance Coverage Works

Comprehensive car insurance works by providing financial protection for your vehicle in the event of non-collision-related damages. Here’s a step-by-step breakdown of how it typically operates:

- Policy Purchase: The first step is purchasing a comprehensive car insurance policy from a reputable insurer. This involves selecting coverage limits, deductibles, and any additional options or riders.

- Premium Payments: Policyholders are required to pay regular premiums to maintain their coverage. These premiums can be paid monthly, quarterly, or annually, depending on the insurer’s terms.

- Incident Occurrence: If an incident covered by the policy occurs (e.g., theft, natural disaster), the policyholder must file a claim with their insurance company.

- Claim Filing: The policyholder provides details of the incident, including any necessary documentation, such as police reports or photos of the damage.

- Assessment and Approval: The insurance company assesses the claim, evaluates the damage, and determines the payout amount based on the policy’s coverage limits and deductibles.

- Payout and Repair: Once the claim is approved, the insurer issues a payout to the policyholder or directly to the repair facility, covering the costs of repairs or replacement of the vehicle, minus the deductible.

This process ensures that vehicle owners are financially protected against a wide range of non-collision-related risks.

Features of Comprehensive Car Insurance Coverage

Comprehensive car insurance policies come with several features designed to offer extensive protection for your vehicle. Here’s a detailed look at these features:

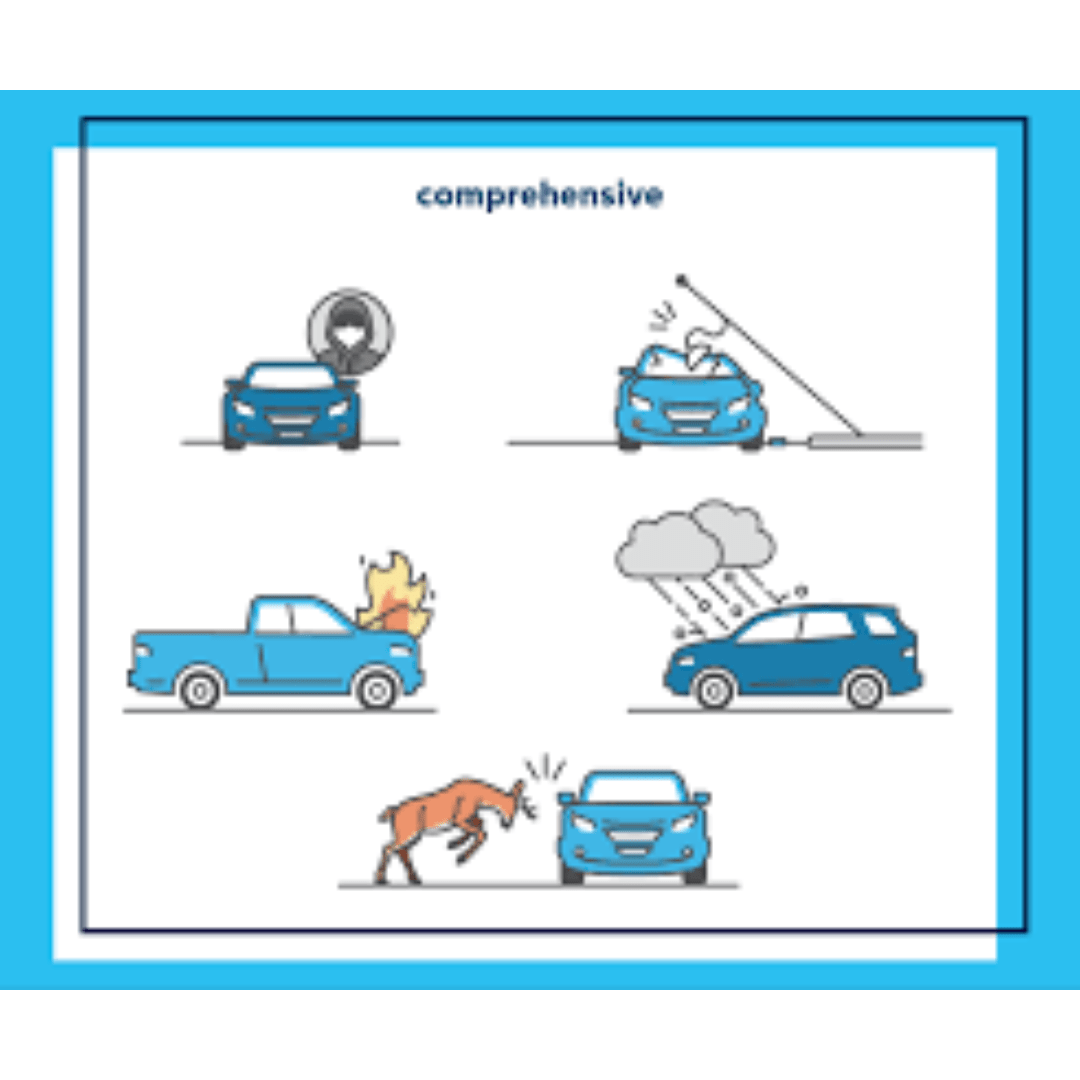

1. Wide Range of Covered Incidents

- Theft: Coverage for the theft of the vehicle and any resulting damages.

- Vandalism: Protection against damages caused by vandalism or malicious acts.

- Natural Disasters: Covers damages from natural events like hurricanes, floods, earthquakes, and hailstorms.

- Fire: Protection against damages caused by fire, whether accidental or intentional.

- Animal Damage: Covers damages caused by collisions with animals or animal-related incidents.

- Falling Objects: Coverage for damages from falling objects such as trees or debris.

2. Customizable Coverage Limits

- Policyholders can choose coverage limits that suit their needs, providing flexibility in the level of protection.

3. Deductibles

- Deductibles are the amount policyholders pay out-of-pocket before insurance coverage kicks in. Higher deductibles typically result in lower premiums and vice versa.

4. Rental Car Reimbursement

- Some policies offer rental car reimbursement, covering the cost of a rental car while your vehicle is being repaired.

5. Roadside Assistance

- Optional coverage for roadside assistance services, such as towing, battery jump-starts, and flat tire changes.

6. Glass Coverage

- Protection against damages to windows, windshields, and other glass components of the vehicle.

7. New Car Replacement

- For newer vehicles, some policies offer new car replacement coverage, providing a brand-new car of the same make and model if the insured vehicle is totaled.

Pros of Comprehensive Car Insurance Coverage

| Pros | Description |

|---|---|

| Extensive Protection | Covers a wide range of non-collision-related incidents, providing robust protection for your vehicle. |

| Peace of Mind | Offers assurance that your vehicle is protected against various risks beyond your control. |

| Customizable | Flexible coverage limits and deductibles allow you to tailor the policy to your needs. |

| Value Preservation | Helps maintain the value of your vehicle by covering repair and replacement costs. |

| Convenience | Includes additional features such as rental car reimbursement and roadside assistance, enhancing the convenience for policyholders. |

Cons of Comprehensive Car Insurance Coverage

| Cons | Description |

|---|---|

| Higher Premiums | More extensive coverage typically comes with higher premium costs. |

| Deductibles | Policyholders must pay a deductible out-of-pocket before coverage applies, which can be a financial burden in the event of a claim. |

| Not Mandatory | Unlike liability insurance, comprehensive coverage is not legally required, leading some to forgo it to save on costs. |

| Potential Overlap | May overlap with other insurance policies or coverage options, leading to redundant coverage and unnecessary expenses. |

| Complex Claims Process | Filing and processing claims can be time-consuming and require extensive documentation. |

Comprehensive Car Insurance Coverage Alternatives

| Alternative | Description | Pros | Cons |

|---|---|---|---|

| Collision Insurance | Covers damages resulting from collisions with other vehicles or objects. | Lower premiums, essential coverage for accidents. | Does not cover non-collision incidents. |

| Liability Insurance | Covers damages you cause to others in an accident. | Legally required, affordable premiums. | Does not cover your own vehicle’s damages. |

| Personal Injury Protection | Covers medical expenses and lost wages for you and your passengers. | Provides medical coverage regardless of fault. | Does not cover vehicle damages. |

| Gap Insurance | Covers the difference between the car’s value and the remaining loan balance. | Protects against financial loss for financed vehicles. | Additional cost, not comprehensive coverage. |

| Uninsured/Underinsured Motorist | Covers damages caused by drivers with insufficient or no insurance. | Protects against uninsured drivers. | Does not cover other types of damages. |

Conclusion and Verdict on Comprehensive Car Insurance Coverage

Comprehensive car insurance coverage offers a high level of protection for your vehicle against a wide array of non-collision-related incidents. It provides peace of mind by ensuring that you are financially protected from unexpected events such as theft, vandalism, natural disasters, and more. While the premiums may be higher compared to basic coverage options, the extensive benefits and features justify the cost for many vehicle owners.

The ability to customize coverage limits and deductibles, coupled with additional features like rental car reimbursement and roadside assistance, make comprehensive car insurance a valuable investment. However, it is essential to weigh the pros and cons and consider your individual needs and budget before making a decision.

Overall, comprehensive car insurance coverage is highly recommended for those looking to ensure their vehicle is well-protected against a broad range of potential risks.

FAQs on Comprehensive Car Insurance Coverage

1. Is comprehensive car insurance mandatory?

- No, comprehensive car insurance is not legally required. However, it is highly recommended for the extensive protection it offers.

2. What incidents are covered by comprehensive car insurance?

- Comprehensive insurance covers non-collision-related incidents such as theft, vandalism, natural disasters, fire, and animal damage.

3. How can I lower my comprehensive car insurance premiums?

- You can lower your premiums by opting for a higher deductible, maintaining a clean driving record, and taking advantage of any discounts offered by your insurer.

4. Does comprehensive insurance cover rental cars?

- Some comprehensive policies include rental car reimbursement as an optional feature. Check with your insurer to see if this is included in your coverage.

5. Can I add comprehensive coverage to an existing policy?

- Yes, most insurers allow you to add comprehensive coverage to your existing auto insurance policy.

6. What is the difference between comprehensive and collision insurance?

- Comprehensive insurance covers non-collision incidents, while collision insurance covers damages resulting from collisions with other vehicles or objects.

7. How do I file a comprehensive insurance claim?

- To file a claim, contact your insurance company, provide details of the incident, and submit any required documentation such as police reports or photos of the damage.

8. Are natural disasters covered by comprehensive insurance?

- Yes, comprehensive insurance typically covers damages caused by natural disasters such as hurricanes, floods, and earthquakes.

9. Does comprehensive insurance cover glass damage?

- Many comprehensive policies include coverage for glass damage to windows and windshields. Check with your insurer for specific details.

10. Can comprehensive insurance be bundled with other types of coverage?

- Yes, comprehensive insurance can be bundled with other types of coverage such as liability and collision insurance for a more comprehensive protection plan.